By Stephen Blewitt and Nathaniel Margolis

After a long period of low inflation, the U.S. experienced a sharp rise in prices starting in 2021, which has only recently begun to ease. The Federal Reserve’s most recent estimate for annual expected inflation over the next 10 years is only about 2.3%, but some economists warn that higher inflation may persist due to continued budget deficits, the potential for higher tariffs, and tighter labor markets.

This surge has reminded investors of the risk inflation poses to long-term financial security by eroding real returns for investors and diminishing the value of investments that fail to account for or respond to it. In this article, we examine how private real assets can play a role in addressing the challenges caused by inflation. Looking at the distinctive characteristics of private real assets, we explore the practical considerations and potential benefits of using them to hedge against inflation.

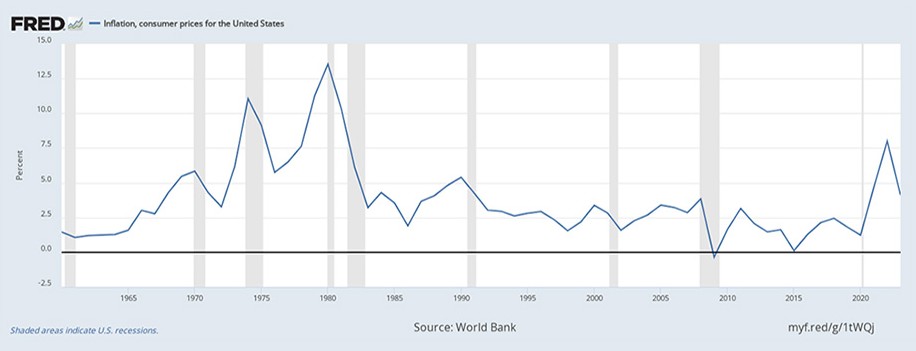

U.S. Inflation 1960–2023

The Challenges of Assessing the Impact of Inflation in Investment Portfolios

Before delving into real assets, their potential to hedge inflation risk, and relevant research findings, we first highlight two key factors investors should consider when evaluating the data presented:

The Federal Reserve, and other Central Banks, changed their monetary policy in the 1980s to combat high inflation. This policy change resulted in decades of low inflation until recently. Because of this long period of stability, there is limited data to evaluate how different asset classes effectively hedge high inflation under the Fed’s current policies. While studies using pre-1980s data shouldn’t be disregarded, understanding how asset classes have performed since the 1980s may provide investors with more relevant insights for decision-making.

Many real assets are tied to operating businesses, and the actions these operators take to preserve, or smooth, profitability can influence how the assets behave as an inflation hedge. For example, an operator may sign tenants to long-term leases to maintain consistent occupancy and protect an asset against economic volatility. While potentially beneficial over the long term, such leases limit an operator’s ability to raise rents and can mute the asset’s capacity to hedge short-term inflation. As another example, an operator may enter supply contracts that stabilize operating costs even in the face of rising prices. These contracts may again preserve profitability and amplify the asset’s ability to hedge short-term inflation. This may be evident if the operator is able to keep their costs to operate the asset steady while passing along price increases to tenants or customers. However, most research on inflation-hedging focuses on asset class performance as a whole, rather than examining the impact of these operational strategies. This gap highlights a need for further study into how such factors influence the inflation-hedging potential of real assets.

What Are Real Assets and How Can They Hedge Against Inflation?

Real assets broadly refer to tangible assets acquired for investment purposes, as well as investments in entities that own and operate such assets. Think real estate, infrastructure, farmland, timberland, and energy-related commodities. While art, jewelry, and similar collectibles are also real assets, we exclude them here due to the lack of a capital markets-based investment framework. Most commodities, except energy, are also excluded since they represent a small portion of private markets, though they may still serve as inflation hedges. Similarly, treasury inflation-protected securities (TIPS) are not considered in this context for two reasons: they are only considered “real” because they are created to deliver a real rate of return, and they are only traded in public markets.

By focusing on real estate, infrastructure, and natural capital, we aim to explore the inflation-hedging benefits of real assets in private markets, where they play a role in diversifying portfolios and preserving wealth and real income.

Real Estate

The investable universe for real estate is large and broadly diversified. Segments of the market include office, retail, multi-family, industrial, healthcare, life sciences, hospitality, and niche areas like storage and recreational spaces. Data centers are a burgeoning segment, combining elements of infrastructure and energy, while single-family residential rentals are expanding as institutional investors acquire or build homes for lease.

Real estate does not provide automatic inflation protection (and in some instances can be negatively affected by inflation), but some of its features make it more likely to serve as a hedge. As prices rise in the broader economy, real estate prices tend to rise too. If a property can take advantage of increasing rents through rent adjustments built into long-term leases, or short-term leases that can be adjusted annually (e.g. apartment buildings), then those properties can be good hedges. In commercial leases, landlords frequently pass all or a portion of their operating expenses to tenants. This means that inflation is less likely to erode the portion of rent that owners receive for occupancy of the property, so-called base rent.

Additionally, if an investor owns a property financed with fixed-rate debt, that portion of their cost structure is unaffected by inflation. In that instance, the investor’s equity value in the property may increase in a rising price environment.

However, these protections depend on maintaining credit-worthy tenants who can meet rent obligations. Periods of increased inflation can be economically turbulent ones, which can strain businesses, leading to tenant defaults and disrupting income streams. The value of inflation-hedging can be lost to general economic volatility and secular changes. We have seen this occur recently with significant declines in the value of office properties as the pandemic affected how organizations use commercial offices.

Infrastructure

Infrastructure assets span a wide range, including power plants, renewable energy projects, energy transmission, telecom assets, toll roads, water systems, transportation systems, ports, and airports, to name a few. These projects can be structured to provide long-term contractual payments backed by strong credit parties. These payments may increase as certain costs do, providing investors with protection against inflation.

Regulated utilities, for example, are often allowed to pass increased costs—such as higher fuel prices—on to customers while maintaining equity returns. This helps insulate the real value of infrastructure investments from increases in costs.

However, some infrastructure assets are more vulnerable to economic downturns. Airports, toll roads, and other usage-based assets may experience declines in revenue during periods of reduced activity or economic volatility. Additionally, stable assets with fixed rents, fixed-rate increases, or rents that lag the market may fall behind when inflation rises faster than expected.

Natural Capital Assets

The World Bank defines natural capital as “the Earth’s living and nonliving natural assets such as soil, air, water, flora, and fauna.” Investments in natural capital address various dimensions, including the costs and risks associated with climate change and biodiversity loss. Many segments of this asset class are now, or may in the future be, available to investors. Here, we look at three well-established natural capital sectors in private markets: energy, timberland, and agriculture.

Energy: Fossil fuels like oil, gas, and coal dominate global energy consumption, though renewables such as solar, wind, hydropower, and geothermal (often considered infrastructure assets) are growing. Energy is used throughout virtually all segments of the U.S. economy and accounted for about 4.8% of the country’s gross domestic product (GDP) as of 2020. This percentage has fluctuated over the past 50 years, ranging from about 5% to 14% of GDP. Price spikes due to overheated economies or energy supply shocks can lead to unexpected energy inflation, often driving up core inflation as producers pass higher energy costs on to consumers.

Timberland: Timber supports multiple industries, providing wood for construction and furniture and pulp for a variety of consumer goods. Demand for wood used in building and durable goods is cyclical, rising and falling with economic trends such as housing demand. Pulp, by contrast, serves more stable consumer needs but faces long-term shifts, such as reduced paper use as digital technologies grow.

Agriculture: Agriculture encompasses a broad spectrum of crops used for livestock feed, protein supply, human food, and other consumables. These include row crops—grown and cultivated annually from seed—and permanent crops, such as fruit and nut trees and vines, which require years of cultivation but provide long-term yields.

Capacity for Inflation Hedging Depends on How Assets Are Operated

The ability of real assets to hedge against inflation depends significantly on how they are managed and operated. Owners can choose to expose their assets to price variability by selling products in the open market without any contracts. This approach allows them to benefit if prices rise faster than operating costs, but also exposes them to losses if prices fall. Similarly, owners can allow operating costs to flow through their income statements unhedged and incur lower profitability during inflationary environments, or benefit when costs decline.

Alternatively, owners may enter contracts with customers in an attempt to preserve their profitability regardless of the economic environment. They can choose to sell their products at a fixed price, for example, or at a price where they pass along some, but not all, of their increased costs to the tenant. In these cases, the asset may provide less of a hedge against inflation to investors.

Ultimately, the decisions and strategies employed by fund managers operating real assets on behalf of investors play a critical role in determining whether these investments serve as effective inflation hedges in the investor’s broader investment portfolio.

We’ll continue this discussion part 2, where we analyze some recent research findings and important considerations for individual investors in the space…stay tuned.

About the Contributors

Learn more about CAIA Association and how to become part of a professional network that is shaping the future of investing, by visiting https://caia.org/