by Daniil Shapiro, CFA, Director, Product Development, Cerulli Associates

Further integrating alternatives into retail investor portfolios means placing the assets in convenient structures alongside public market exposures.

A relative nearing retirement recently shared a snapshot of their investments, and topping the list is a credit interval fund from a private capital manager that would have played no role in this portfolio a decade ago. Despite gripes with the “democratization” label, it must be acknowledged that alternatives managers have done a tremendous job of making private capital exposures accessible to a much larger investor base in recent years.

Key intermittent liquidity structures (defined as non-traded REITs, non-traded BDCs, interval funds, and tender offer funds) are gathering flows from a broad pool of investors. Interval fund product, specifically, is perceived as easier to access and similar enough to the mutual fund structure while offering investors access to in-demand private credit and other strategies. Minimum investments in interval funds are (for non-institutional share classes) in the $2,500 to $10,000 range, establishing them as a gateway to alternatives access.

On the back of strong education efforts and media coverage, the benefits of alternative investments exposures are increasingly attractive to investors. This is especially true in an environment of growing discomfort with more concentrated public equity markets and low returns in public fixed income, particularly amidst a growing perception that neither is currently representative of the broader economy. Private credit in particular has been attractive to investors due to its ability to offer an exposure perceived as safe and offering greater income than that available in public markets—one that plays well to those planning for retirement.

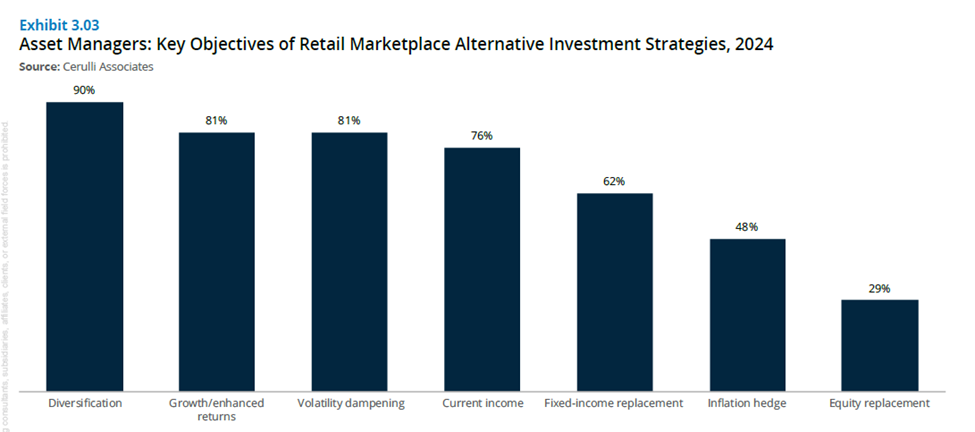

Exhibit 1

Alternative investments are increasingly being used to do more, providing a complement and replacement to fixed income and equity exposures.

Market Developments

Several 2024 filings hint at a future where public and private market exposures will live side by side. This is not new, but the greater sophistication of participants and their heft behind the exposures is. Capital Group and KKR have filed to launch two interval funds, the Capital Group KKR Core Plus+ and Multi-Sector+, that blend public credit and private credit exposures. Both funds aim for a 60/40 public vs. private split. The funds will have a private capital focus on direct lending and asset-based finance, while the latter tilts toward higher-yield corporate debt and securitized debt on the public side. Both are excellent examples of how private and public credit exposures can complement one another to create a more holistic solution that will be attractive to advisors initiating use of alternatives. Pairing a corporate bond exposure with a direct lending exposure is a sensible approach. Importantly, the latter should be less sensitive to interest rate changes, providing a form of diversification. The two exposures are forms of lending initiated by two different types of firms (banks vs. alternative managers funded by private capital) and investors who want exposure to lending to companies will likely want to take part in both.

Such combinations of traditional public exposures and alternative versions should, as the industry grows, become more commonplace, further allowing a wide variety of investors to access alternatives via simpler structures and simultaneously integrating alternatives into products in a way that doesn’t separate the exposure solely based on who originates it. Moving a step beyond to packaging such solutions into the ETF structure can be another path forward, as suggested by a September 2024 filing from State Street in partnership with Apollo.

Illiquid Alternatives in the ETF Structure

The placing of an illiquid exposure into the ETF structure is perceived as heresy in the ecosystem that evolved based on offering low-cost access to public markets. But, increasingly, this is not what the $10 trillion+ ETF industry is today. Beyond the now fast-paced uptake of active product, some of the fastest-growing categories offer access to more complex derivatives-based strategies that take structured notes and variable annuities head-on, while some of the largest ETF issuers now offer cryptocurrency. Much investor attention (if not flows) in the ETF ecosystem goes to leveraged/inverse product and short-term trading exposures that, in prior lives, established ETF issuers have sought to strip of the ETF label. As the ETF emerges among investors and advisors as the structure of choice for accessing the greatest variety of exposures, alternative investments will have a natural role to play.

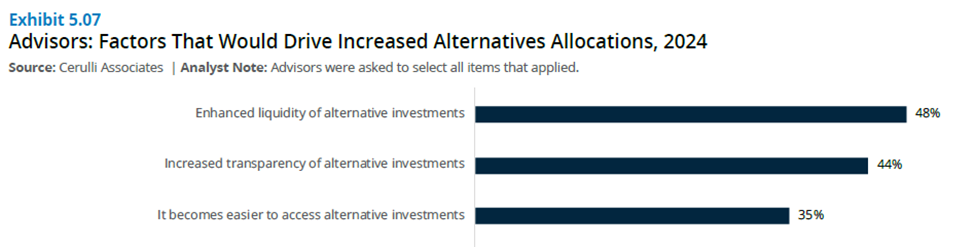

Exhibit 2

The top three factors that would drive advisors toward greater alternative investments allocation include greater liquidity, transparency, and easier access, which would all be aided by access through the ETF structure.

Of course—and especially as relates to the ETF structure—the above is easier said than done, as private capital exposures do not have the liquidity of public markets exposures. They also have less frequent valuations, which adds uncertainty, especially within the confines of a product where authorized participants arbitrage values to the penny.

One potential avenue and a good start is including a small allocation to illiquid product within the confines of the 1940 Investment Company Act, where 15% of the exposure of the fund can be illiquid (defined as sellable within seven days without causing significant change to the market value of an investment). Cerulli believes that even a 10% private capital allocation within a diversified ETF exposure is a meaningful addition because it solves the advisor and investor problem of alternatives being more difficult to access. It also removes an important mental block associated with alternative exposures, wherein newcomers perceive them as riskier and very different from the traditional exposures in which they have far fewer qualms about investing. Cerulli expects such products to carry a risk of diverging from the NAV in an adverse market environment, but it should be mitigated by the limited size of the allocation relative to other holdings and the competitiveness of the marketplace.

Adding Liquidity to Private Capital Exposures to Increase the Allocation Beyond 15%

Over time, Cerulli expects such liquidity to emerge for some private capital holdings, in turn allowing such exposures to make up more than 15% of an ETF product. It’s likely that this will take place first on the private credit side. According to industry media, firms including JPMorgan, Golub, Apollo, and Antares are building trading desks that make direct lending loans more liquid. It wouldn’t be shocking to see such liquidity also emerge for individual private company equity stakes to the extent that some private companies (e.g., SpaceX) have valuations in the hundreds of billions and transactions are already actively facilitated via specialist brokers. It’s not clear whether the private credit trading desks being stood up will be able to support ETF product in the near term, but the undertaking is similar to the emergence of senior loan and CLO trading desks that led to the packaging of those exposures into mutual funds and ETFs.

This effort will not be without challenges, as some managers will not want the loans they underwrite to be traded—and sourcing a wide variety of loans will remain difficult, resulting in the universe being limited to the largest and most liquid components. A functional market will only exist when a private loan or private company allocation can receive bids from multiple competing counterparties.

Takeaways

The growing breadth of alternative investments exposures and the use of the ETF structure to increasingly provide access create a case for placing the former into the latter. The effort brings risks and will require an investment in building trading desks for alternative product and standing up new policies and procedures. It will require great care overall, but it is worth it for the benefits it offers in providing investors with better rounded solutions in a structure they like. In the long term, Cerulli believes that the growth of such exposures can revolutionize private capital markets. First, they will make these investments more commonplace, and second, they will add a layer of competition. When the largest individual private capital exposures (loans and private company stakes) are easily accessible and liquid, the bar is higher for managers offering access to the same through less liquid structures.

About the Contributor

Daniil Shapiro, CFA is part of Cerulli’s Product Development practice, where he works on the identification, analysis, and reporting of asset management industry trends with a focus on exchange-traded funds (ETFs) and alternative investments.

Learn more about CAIA Association and how to become part of a professional network that is shaping the future of investing, by visiting https://caia.org/